With “digital’ being the buzzword in modern India, one sector that is expected to experience multi-fold growth in the coming decade is “Data Centers”. Data Centers (“DC”) are the spinal cord of the digital world, providing the infrastructure for storing and processing the vast amounts of data generated every day. The primary purpose of a data center is to store, process, and manage the massive amounts of data generated by our increasingly connected digital world. India is the fastest growing digital economy in the world. In 2014, the digital economy was around 4.5 per cent of the GDP and today it is 11 per cent. By 2026, digital economy will account for 20 per cent or one-fifth of the Indian GDP.

Thanks for reading WealthYatra’s Newsletter! Subscribe for free to receive new posts and support my work.

Growth Drivers for Data Centers:

· India’s digital economy is expected to register a six-fold growth, reaching USD1 trillion by 2030, driving the quantum acceleration of data center clusters across the country.

· Growth of AI based applications, greater penetration of IoT, Big Data Analysis and Analytics, Over the Top (OTT) video consumption, online gaming due to the roll out of 5G mobile networks, global capability centers (GCC) and govt’s plans to connect village panchayats with optical fiber by 2025, Digital Banking Units (DBUs), and the National Digital Health Ecosystem are key drivers.

· Mass adoption of cloud computing by global hyperscalers such as Amazon Web Services (AWS), Microsoft, Google and NTT STT looking to build their own Built to Suit (BTS) data center facilities in India.

· Data localization Regulations: Digital Personal Data Protection Bill of 2023 that limits cross-border data storage, encouraging local storage of country’s data is a huge driver for in-house data storage.

· Rising demand for edge data centers driven by the technologies mentioned above in Tier II and III cities

Current infrastructure:

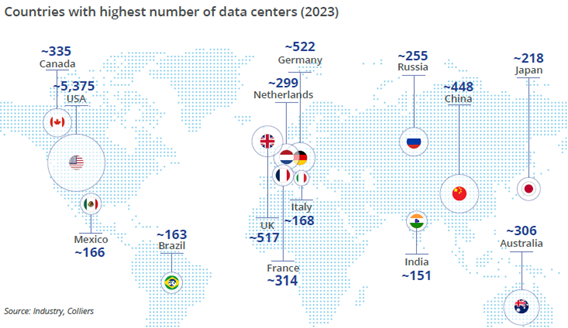

India has become one of the fastest growing data center markets in the APAC region, and ranks 14th globally in its data center inventory

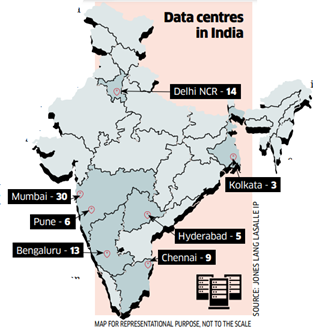

Mumbai, Chennai, Bangalore and Delhi-NCR are the established tier-I DC markets in India. These cities accounted for about 87% of the country’s DC stock as of H1 2023. Mumbai continues to be the most prominent DC market in the country accounting for more than half of the total DC network.

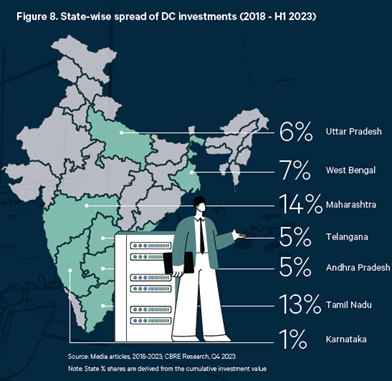

Hyperscale DCs dominated majority of these investments with a share of about 89%, while colocation DCs contributed to the rest 11%. The top states that dominated the cumulative investment commitments include Maharashtra, Tamil Nadu, West Bengal and Uttar Pradesh.

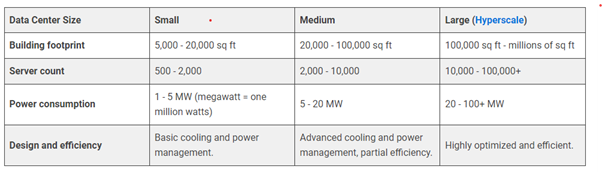

Types of Data Centers:

Demand potential:

Data Storage requirement is expected to exceed 2000 MW IT Load Capacity by 2025. By 2029, the Data Centre India Market will be worth $2.84 billion, growing at a pace of 10.8% year between 2022 and 2029, predicts Maximise Research.

A recent report by Google, Bain, and Temasek predicts that the Indian Internet economy will reach 1 trillion by 2030. The government is aware of this huge potential and has taken proactive steps and policies to support the Data Centre industry. The government has granted Data Centers and energy storage systems special status in the budget for 2022–2023, making it simpler for them to get permissions and financial backing.

Overall, 5000 MW of capacity involving investments of Rs 1.6 lakh crore are likely to be added in the next six years. Majority of the upcoming investments are geared towards meeting high demand in co-location services. Business conglomerates with the likes of Adanis and Hiranandanis (Yotta Data Services) are jumping into this space by building infrastructure with the help of some tech partners, and opting for the co-location or colo model.

Regulatory & govt support:

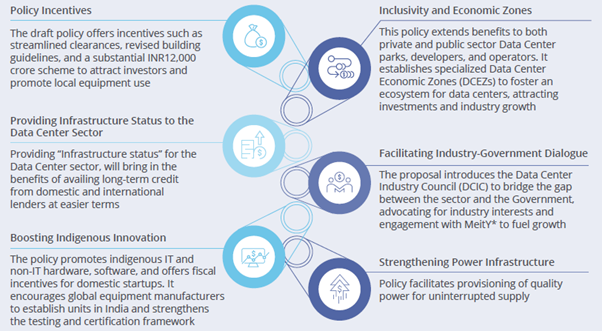

The Ministry of Electronics and Information Technology (MEITY) introduced the draft Data Centre Policy in the year 2020 in order to facilitate effective data center capability for India. The primary reason for the policy was to lay out a framework including various structural / regulatory interventions, investment promotion in the sector, possible Incentivization procedures along with the institutional mechanism required for the governance.

This draft policy combined with India’s Digital Personal Data Protection Bill of 2023, introduced clear rules advising organizations to handle people’s personal information and data processing both within India and outside. Data collected online or offline, and later digitized in India, as well as foreign companies offering goods or services within India come under the ambit of this bill. Along with data protection, the bill also limits cross-border data storage, encouraging local storage of country’s data.

In addition to the centre’s initiative, a host of states have announced important policy initiatives to grab a share of the growing pie

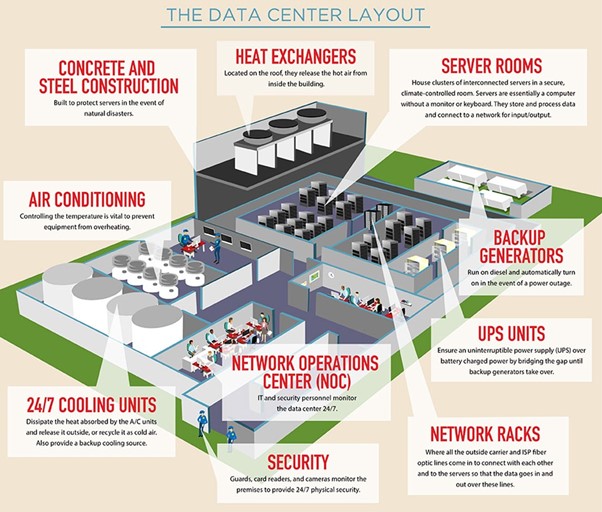

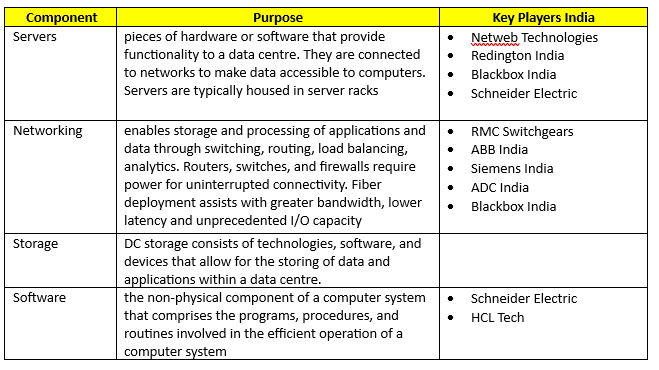

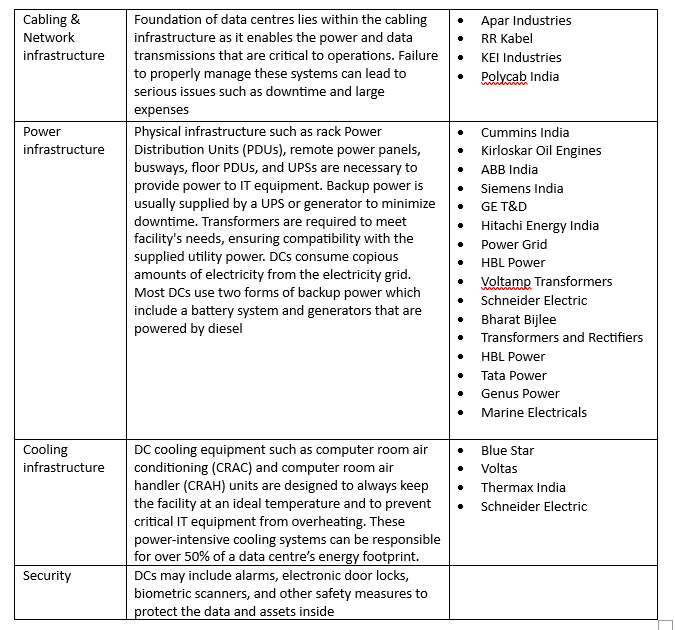

Data Centre Components & key players:

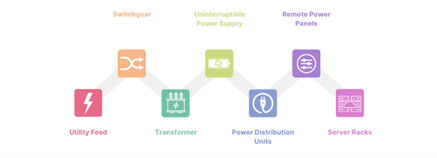

A high-level Data Centre layout is depicted below:

The following table highlights the key components of DC and key listed players in India.

Data Centre Key EPC & Infra Players

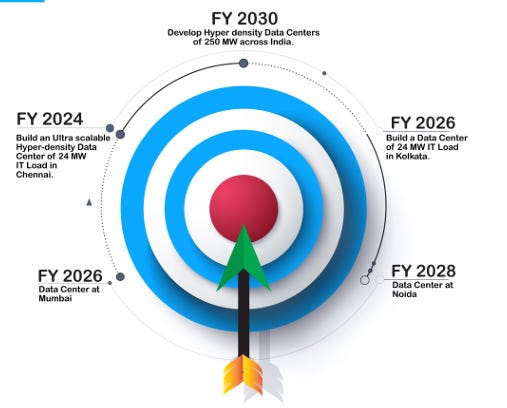

· Techno Electric & Engineering Company Ltd. (TEECL) is one of India’s most prominent power-infrastructure company. Specializing in Engineering, Procurement, and Construction (EPC), asset ownership, operations, and maintenance services, TEECL operates in three key industry segments of power generation, transmission, and distribution. In 2021 TEECL ventured into the DC domain by providing businesses with ultra scale hyper-density data center infrastructures. TEECL offers end to end DC solutions – from land acquisition and site assessment study to design and engineering, civil, structural and electro-mechanical works including power intake solutions works, commissioning and obtaining statutory approvals

TEECL’s DC vision:

· Anant Raj Ltd – a real estate developer through its wholly owned subsidiary Anant Raj Cloud Pvt. Ltd plans to develop Tier III and Tier IV DC up to 150 MW IT Load with minor modifications to the existing ARL IT Park Buildings in Haryana. The company, which has an alliance with Telecommunication Consultants India Limited (TCIL) for its DCs, will provide cloud services, managed services and security services of the cloud to the prospective clients.

· Tata Communications has 26 per cent stake in ST Telemedia Global Data Centers (India) Pvt Ltd, (the Indian subsidiary of the Singapore-based STT GDC), which plans to invest a billion dollars in India over the next 3-4 years to expand its data centers in the country. The company today has 300 MW of data centers, including 100 MW under construction and plans to double the capacity every four years, in the foreseeable future.

· Indian engineering conglomerate – Larsen & Toubro as a part of its Digital Service and e-Commerce platforms provides end-to-end Data Center, Multi-Cloud services, Cloud Managed services, Security Services and Application Integration services with single-point responsibility and has set up state-of-the-art Hyperscale Data Centers at multiple locations in India, starting with Mumbai and Chennai.

In addition, other peripheral players namely – Commercial Real Estate players & Infrastructure players In Steel & Cement, and EPC players in construction will stand to benefit from the boom in DCs in India. For example, DCs offer risk adjusted yields of approximately 16 to 17%, outperforming core office assets at 8-9%.

Critical Infrastructure:

It is important to note though that the Power and Cooling infrastructure remains critical to the whole DC ecosystem. Power infrastructure remains the life blood for DCs as storage, optimizing performance, minimizing disruptions, and mitigating security risks are dependent on power. DCs also require a significant increase in the power needs. For example, Electricity used by data centers in Ireland has risen by 400% since 2015, accounting for nearly a fifth of national consumption.

The table below provides a rough overview of DC power requirements:

DC Power Distribution:

DC cooling systems are essential for maintaining the ideal operating conditions within data facilities. Temperature and humidity levels are controlled well by these systems. It ensures peak performance, prevents downtime, extends the life of equipment, saves energy and creates a comfortable work environment. As cooling technology changes from standard CRAC and CRAH units to direct chip or two-phase immersion or geothermal or microchannel/micro connective liquid to calibrated vector cooling, performance and efficiency are also expected to increase in the future.

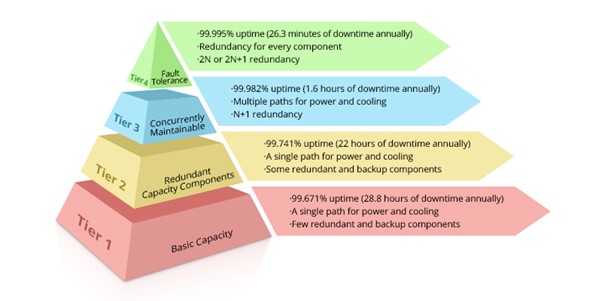

Additionally, downtime in DC is extremely costly in terms of money and reputational clout. Globally, on an average downtime costs small businesses anywhere from $137-$427/minute while larger companies suffer a cost of $5,600-$9,000/minute. DC tiers are therefore a helpful way to understand a number of details about DC facilities. DCs are ranked from I to IV, with I offering the lowest performance and IV the highest. This means that tier I DCs experience the most downtime while tier IV centers experience the least.

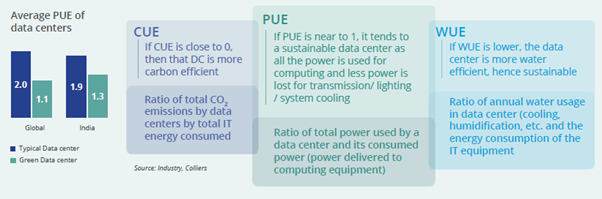

The contribution of DCs towards sustainability can be determined by its three primary components – Power Usage Effectiveness (PUE), Water Usage Effectiveness (WUE) and, Carbon Usage Effectiveness (CUE).

Key Challenges:

· Based on rating agency – ICRA’s analysis, increase of revenue and better absorption of fixed costs, operating margins in the near term are expected to be in the range of 43-44% but DCs will be forced to be in continuous capex mode and increasing competitive intensity would exert margin pressures for incremental business which may be eventually be funded by large debt funded capex plans. ICRA further estimates cost per megawatt (MW) of setting up DCs has also been rising with costs escalating to levels of Rs 60-70 crore per MW from average per MW cost of Rs 40–Rs 45 crore. Other challenges include project execution, in terms of land and equipment availability and management of vendor ecosystem

· Data centers use around 3% of the world’s electricity, producing 1% – 2% of all greenhouse gas (GHG) emissions. Going forward DCs are projected to consume 8 percent of electricity worldwide by 2030. The quantity of energy needed to cool the computers and equipment in data centers makes them power hogs. Uninterrupted power supply, availability of copious amount of clean water, protection of grid structure from cyber threats, disposal of electronic waste that does not impact environment and the use of renewable energy to reduce carbon footprint will remain critical.

· Use of advanced technologies for cooling, increasing efficiencies to reduce overall energy consumption and spreading out of computing resources will further help in the sustainability of the overall ecosystem of DCs. Given the power consumption of DCs in India is expected to reach nearly 5 gigawatts over next six to seven years, the Indian government has recognized the need and importance of green DCs and has taken steps to encourage their development. MEITY has launched a program called the “Green Base Data Centre” scheme, which provides incentives for companies to build energy-efficient and environmentally friendly DCs.

· Cyberattacks are an increasingly relevant threat for Small and Medium Businesses and therefore business continuity is a major concern for decision makers and executives. After all, the cost of downtime is significant and oftentimes crippling. It is therefore important for businesses to choose the right Tier to host the most valuable information. Costs to therefore hosting in such tiers could be an issue.

Conclusion:

· India’s growing digital economy. vast landmass, skilled IT workforce, and growing demand for digital services across every section of the society will drive the demand for the DC market in the coming decade.

· A common investor has a wide spectrum of opportunities in this space although valuations in the recent run up in the equity markets of many players in this space remains elevated.

· DCs growth is a decadal theme and investors should look to exploit any opportunities in dips and look to target suppliers and established players who provide the critical infrastructure and those addressing Tier III and IV systems.

· During 2020-September 2023, DCs accounted for about 54% of total private equity investments. Real estate and construction costs constitute 30-40% of the total DC development cost. Owing to the high volume of investments required, large investors such as Blackstone, Brookfield, Capitaland and Kotak have been primarily infusing funds in DC space in India. An alternate way of looking at investment opportunities would be look at commercial REITS focused on DC properties or through private equity investments in this area. Kotak’s Data Centre Fund by Kotak Alternate Assets, which is managed by Kotak Investment Advisors, is set to invest a whopping $800 million in the development of 5-7 large data center assets across key property markets in India.

Sources:

· CBRE Research report – From Bytes to Business: India Data Centre Market Powering Progress in 2023, Dec 2023

· Colliers CII India Center – India Data Centers, Oct 2023

· Nasscom Key Findings Data Centers

· ICRA: Data Centers, India: A hotspot of data center investments, Oct 2023

· Other publicly available media sources, Company Annual Reports and Investor Presentations

Thanks for reading WealthYatra’s Newsletter! Subscribe for free to receive new posts and support my work.